Learn how credit cards work in the USA in simple terms. Understand billing cycles, APR, interest math, rewards, fees, credit utilization, and how cards affect your credit score.

Introduction

Okay, real-life moment.

You’re in the U.S. You order food. Maybe a burger. Maybe sushi. Maybe one of those “I’ll just get something light” meals that somehow costs $22. You tap your card. Beep. Done.

You walk away thinking, cool, paid.

But technically… you didn’t.

You borrowed.

That tiny beep? That’s you taking a short-term loan from a bank without paperwork, awkward conversations, or anyone saying the word debt. It’s smooth. Frictionless. Almost suspiciously easy.

And here’s the part people don’t realize early enough — credit cards in America are not just payment tools. They are tied to your credit score, which affects apartments, car loans, home loans, insurance costs, and sometimes even job screenings.

So that little card you used to buy fries? It’s quietly connected to your future.

Let’s unpack this whole system properly, like real people.

What Is a How Credit Cards Work in the USA?

A credit card is basically borrow-now, pay-later access.

Not your money. The bank’s money.

You’re given a credit limit — say $2,000. That’s the maximum the bank trusts you to owe at any time.

You spend $200 → you now owe $200.

You pay it back → you can borrow again.

This keeps repeating. That’s why it’s called revolving credit.

It feels like spending. But it’s technically boring every single time.

How Credit Cards Work

Let’s walk through the real flow.

Step 1: You Make a Purchase

You tap your card at a restaurant for $50.

Step 2: The Bank Pays

The restaurant gets paid quickly by your bank through the payment network.

Step 3: You Owe the Bank

That $50 is now your debt.

Step 4: Billing Cycle Closes

At the end of your billing cycle (usually about 30 days), the bank sends a statement listing everything you spent.

Let’s say your statement shows:

| Purchase | Amount |

| Groceries | $120 |

| Gas | $60 |

| Dining | $80 |

| Online order | $40 |

| Total | $300 |

Now you have choices.

The Grace Period

Most credit cards give about 21–25 days after the statement closes.

If you pay the full $300 before the due date…

You pay $0 interest

Free borrowing.

If You Don’t Pay in Full…

Let’s say you only pay $50 and leave $250.

Now interest starts.

This is where APR (Annual Percentage Rate) comes in.

Real-Life Interest Math (The Part Nobody Shows You)

Let’s say your APR is 24%.

That’s yearly, but interest is calculated daily.

Daily rate = 24% ÷ 365 ≈ 0.065% per day

You carry a balance of $1,000.

Daily interest =

$1,000 × 0.00065 = $0.65 per day

In 30 days:

$0.65 × 30 = $19.50

That gets added to your balance.

Next month, interest is calculated at $1,019.50.

That’s compounding.

Types of Credit Cards

H3: Rewards Credit Cards

These give cashback, points, or travel miles.

Example:

You spend $1,000 in a month.

Your card gives 2% cashback.

You earn $20.

Nice… unless you carried a balance and paid $30 in interest. Then you lost money.

Rewards only work if you avoid interest.

Secured Credit Cards

Designed for beginners or people rebuilding credit.

You deposit money, say $300. That becomes your limit.

You’re borrowing against your own deposit. Lower risk for the bank.

Eligibility / Requirements

To get a U.S. credit card, banks usually check:

- Income

- Existing debt

- Credit history

- Identity verification

No history? You may start with a secured card.

Fees, Charges & Costs

Interest isn’t the only cost.

| Fee Type | Example |

| Late fee | $30–$40 |

| Annual fee | $0–$550+ |

| Foreign transaction | ~3% |

| Cash advance fee | 3–5% + high APR |

Cash advances are brutal. Interest starts immediately.

Pros and Cons

Pros

- Builds credit

- Rewards

- Fraud protection

- Convenient

Cons

- High interest

- Easy to overspend

- Debt stress

- Hidden fees

It’s a tool. Not free money.

Credit Card vs Debit Card

| Credit Card | Debit Card |

| Borrowed money | Your money |

| Builds credit | Doesn’t build credit |

| Interest possible | No interest |

| Strong fraud protection | Varies |

Common Mistakes to Avoid

Only paying minimums

Maxing out cards

Missing due dates

Ignoring statements

Chasing rewards in debt

Been there? A lot of people have.

Credit Utilization — The Silent Score Factor

This one sounds technical, but it’s actually simple math.

Credit utilization = how much of your credit limit you’re using

Formula:

Balance ÷ Credit Limit × 100

Let’s run numbers.

You have:

Credit limit = $1,000

Balance = $500

Utilization = 500 ÷ 1,000 = 50%

That’s considered high.

Experts usually recommend keeping utilization below 30%, and under 10% is excellent.

Why It Matters

Lenders see high utilization as a sign you might be financially stretched.

Even if you pay on time.

It’s not just about if you pay — it’s also about how much you owe compared to what you’re allowed to borrow.

Real-Life Comparison

Person A:

Limit = $5,000

Balance = $500

Utilization = 10%

Person B:

Limit = $1,000

Balance = $500

Utilization = 50%

Same debt. Very different credit score impact.

Credit Score — Your Financial Reputation Number

In the U.S., your credit behavior turns into a score between 300 and 850.

Main components:

| Factor | Approx. Weight |

| Payment history | 35% |

| Amounts owed (utilization) | 30% |

| Length of credit history | 15% |

| Credit mix | 10% |

| New credit inquiries | 10% |

Miss a payment? The score drops fast.

Build a good history? The score rises slowly.

Kind of like trust in real life.

Real-Life Impact — Renting an Apartment

This surprises people.

Many landlords check credit scores before approving tenants.

Low score? You might need:

- A higher deposit

- A co-signer

- Or you might get denied

You could have money in the bank, but no credit history? Still a problem.

Credit is a trust record, not just a debt record.

Real-Life Impact — Car Loans (With Math)

Let’s say two people buy a $20,000 car.

Person A — Good Credit (5% APR)

Loan = $20,000

Term = 5 years

Monthly payment ≈ $377

Total paid ≈ $22,620

Person B — Poor Credit (15% APR)

Monthly payment ≈ $476

Total paid ≈ $28,560

Difference = $5,940 more

Same car. Different credit scores.

Real-Life Impact — Mortgages

Now imagine a home loan.

A 1% difference in mortgage rate on a $300,000 loan can mean tens of thousands of dollars over time.

That’s why credit card habits today quietly affect huge costs later.

The Debt Spiral Example

Here’s how people get stuck.

You owe $3,000

APR = 24%

Minimum payment = $90

Interest per month ≈ $60

You pay $90 → only $30 reduces debt.

You’re barely moving the balance while interest keeps building.

That’s how debt lingers for years.

The Psychology of Credit Cards

Swiping doesn’t hurt like handing over cash.

No physical money leaves your hand. The “pain of paying” is delayed.

You think, “I’ll handle it later.”

Later includes interest.

This is why awareness matters more than income level.

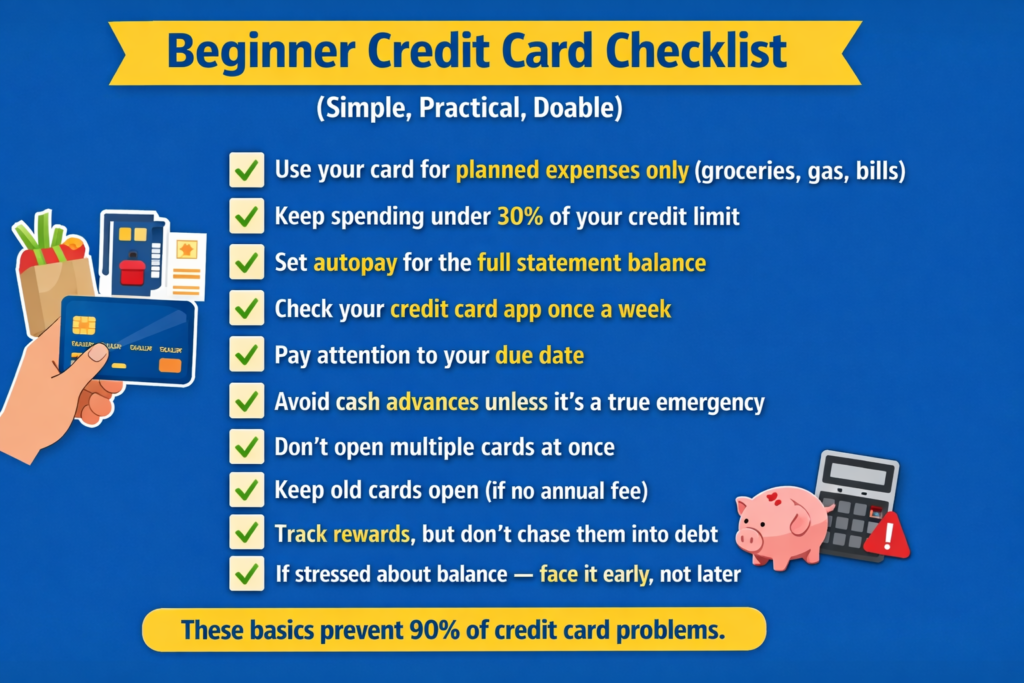

Smart Usage Strategy

If someone said, “Okay, what’s the safe way to use this?”

Here’s the simple version:

Pay full statement balance every month

Keep utilization under 30%

Use autopay for minimum as backup

Track spending weekly

Ignore your credit limit as spending power

These habits prevent most problems.

When Trouble Usually Starts

It’s rarely luxury shopping.

Often it’s:

- Medical bills

- Car repairs

- Job gaps

- Unexpected travel

Life events + high APR = long-term debt.

Early Warning Signs

Paying only minimums

Avoiding looking at statements

Using one card to pay another

Relying on credit for everyday basics

These are signals to adjust quickly.

Step-by-Step Guide for Your First Credit Card

If someone asked me, “I just got my first card. What’s the safest way to use it?” I’d keep it simple.

Step 1 — Use It for One Category Only

Pick something predictable. Like groceries.

Example:

Monthly groceries = $300

Your credit limit = $1,000

Utilization = 30%

That’s a safe zone.

Step 2 — Pretend It’s a Debit Card

Only spend money you already have in your bank account.

So when the bill comes, it’s not panic — it’s just transferring money you already planned to spend.

Step 3 — Turn On Autopay

Set autopay for the full statement balance.

This prevents missed payments, which are one of the fastest ways to hurt your credit score.

One late payment can stay on your report for years.

Step 4 — Check Your Balance Weekly

Not obsessively. Just awareness.

Look at:

Balance

Due date

Spending pattern

This prevents the “I didn’t realize it got that high” moment.

Deep Dive — How Rewards Cards Really Work

Rewards cards look like free money.

But here’s the reality: they’re funded by merchant fees and interest paid by people carrying balances.

Let’s run the numbers.

You earn 2% cashback.

Spend $1,000 → earn $20.

But if you carry that balance and pay $25 in interest?

You lost $5.

Rewards only benefit people who avoid interest completely.

Travel Rewards Example

Airline points are often worth around 1–1.5 cents per point.

If you earn 50,000 points:

Value ≈ $500–$750

Nice vacation.

But not if you paid $600 in interest to earn it.

Getting Out of Credit Card Debt

If you already have debt, rewards don’t matter. Strategy does.

Method 1 — Avalanche Method

Pay extra toward the card with the highest interest rate.

This saves the most money.

Method 2 — Snowball Method

Pay off the smallest balance first.

This builds psychological momentum.

Example

You owe:

Card A — $1,000 at 25% APR

Card B — $3,000 at 18% APR

Avalanche → focus on Card A first.

Snowball → focus on smallest balance first.

Both work. Consistency matters more than the method.

Balance Transfers — A Temporary Reset

Some cards offer 0% APR for 12–18 months.

You move debt to that card and stop interest temporarily.

Example:

Debt = $5,000

APR = 24%

Interest per year ≈ $1,200

Transfer to 0% → you save that interest.

But only helpful if you actually pay it down during the promo.

How to Improve Your Credit Score

Credit scores improve from patterns, not tricks.

The Big Four Rules

- Pay on time

- Keep balances low

- Keep old accounts open

- Don’t open many new accounts at once

Real Score Improvement Example

Person had:

Score = 620

Utilization = 80%

They paid balances down to 20%.

The score rose to around 680–700 over time.

Utilization changes can move scores faster than people expect.

How Long Negative Marks Stay

Late payments → up to 7 years

Collections → up to 7 years

Bankruptcy → longer

But impact fades over time with good behavior.

When Credit Cards Are Helpful

Building credit history

Travel rewards

Fraud protection

Emergency flexibility

When They’re Not

Impulse spending issues

Only paying minimums

Already deep in debt

In those cases, debit cards or cash systems help more.

The Mindset That Changes Everything

This is the shift:

Your credit limit is not spending power. It’s a risk ceiling.

People who treat limits like goals struggle.

People who treat limits like guardrails stay in control.

FAQs

1. Do I really need a credit card in the USA?

Not technically. You can live using debit cards and cash. But in real life? Credit history makes things easier — renting apartments, getting car loans, sometimes even setting up utilities.

2. What’s the safest way to use a credit card?

Simple — spend only what you already have, and pay your full statement balance every month. That keeps interest at zero and builds credit safely.

3. What happens if I only pay the minimum payment?

You avoid being late, but interest keeps growing on the rest. That’s how small balances turn into long-term debt. Been there? A lot of people have.

4. Does carrying a balance help my credit score?

Nope. That’s a myth. You don’t need to pay interest to build credit. Low balances and on-time payments are what matter.

5. What is a good credit score in the U.S.?

Generally, 670+ is considered good. Over 740 is very good. Over 800 is excellent. Higher scores usually mean better loan rates.

6. Why does my score drop when I use my card a lot, even if I pay on time?

That’s credit utilization. If you use a large percentage of your limit, lenders see more risk. Keeping balances low helps your score.

7. Are credit card rewards actually worth it?

They can be — if you pay in full. But if you carry debt, interest usually wipes out any rewards.

8. What’s a secured credit card?

It’s a starter card where you put down a deposit that becomes your credit limit. It’s useful for beginners or rebuilding credit.

Final Thought

Credit cards in the U.S. are tools built inside a profit-driven system.

They don’t judge you. They don’t warn you loudly. They just follow math.

If you understand the math… you stay in control.

If you don’t… the math controls you.

Disclaimer

This article is for educational purposes only and not financial advice. Credit card terms, rates, and policies vary by issuer and individual situation. Always review official agreements and consult a qualified financial professional before making financial decisions.